Buy Property in Singapore: Fly with Singapore Airlines

Planning to buy property in Singapore in 2026? Discover how taking a Singapore Airlines flight can enhance your property investment journey. Explore insights from City of Blocks Editorial on the best strategies for property investment.

6/1/20264 min read

Once a favorite move for HNW portfolios. Now? It depends entirely on who you are.

Many have heard about Singapore Airlines — the crisp service, the Champagne at 40,000 feet, the quiet hum of A380 engines over the Bay of Bengal.

For years, a business class ticket was more than a flight. It was the first step in a wealth strategy.

High-net-worth individuals would fly into Changi, spend a weekend viewing condominiums, sign an Option to Purchase, and fly home with a multi‑million dollar asset added to their portfolio.

No complicated visa. No local partner. Just a lawyer, a bank, and a suitcase.

That era is over.

But not for everyone.

Why Singapore still works

Despite global turmoil — including the ongoing conflict in Iran — Singapore's economy remains resilient. Singapore's full year GDP grew by 5% and for Q1 2026, GDP grew by 6%. Impressive nevertheless for a nation with 6 million population. The resilience for Singapore is not accidental. Seeds were planted a good 40 years ago, just like the Garden City or City in the Garden that it is now known for.

This is not accidental. Singapore practices long-term planning with agile execution — firm 50-year visions, but flexible enough to pivot when disruptions hit. For a property investor, that means stability without brittleness.

The "Great Wall" of Singapore

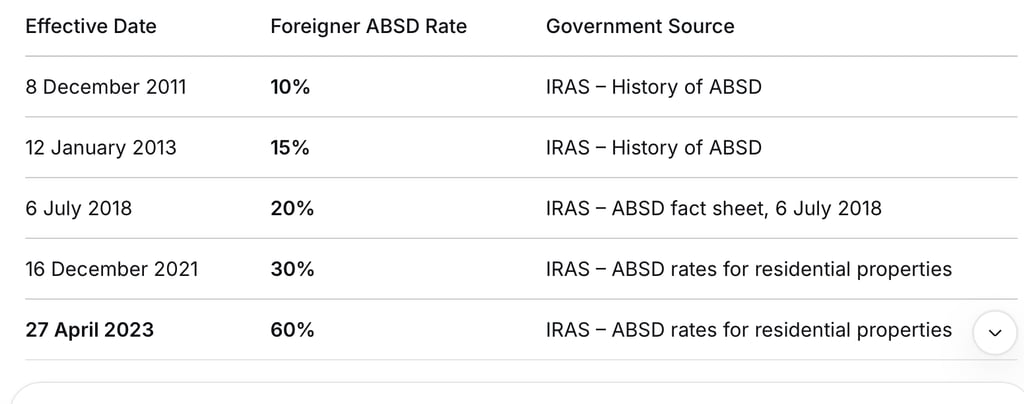

In April 2023, the government raised Additional Buyer's Stamp Duty for foreigners to 60%. This makes it the highest stamp duty in the world. Pretty much in line with the rest of the polices, like how they are controlling the volume of cars in Singapore with the Certificate of Entitlement (Going for a cool SGD$100,000) to own a car for 10 years in Singapore.

A S$2 million property suddenly cost over S$3.2 million upfront for most foreigners.

The math broke. Foreign buying plunged. Certain key districts in Singapore saw the decline in demand from foreigners.

But here is what most people do not realise: it depends on who you are.

Here is a short history article for City of Blocks tracing foreign property buying in Singapore — before, during, and after the ABSD era.

Foreign buyers in Singapore: A short history before and after ABSD

From safe-haven darling to 60% wall. How policy changed the game.

Before ABSD: The golden years (1990s–2011)

Singapore's residential property market has long been a magnet for foreign buyers. The reasons are timeless: political stability, rule of law, a transparent legal system, no capital gains tax, and a currency that holds its value.

The 1996 boom

Foreign buying first hit the headlines in the mid-1990s. In 1996 — the peak of that cycle — foreigners purchased 2,531 private residential units, representing approximately 16.8% of the market.

The Indonesian buyer was king. Wealthy families from Jakarta would fly in for medical check-ups at Mount Elizabeth, shop on Orchard Road, and pick up a condominium in Districts 9 or 10 as a holiday home.

The 2005–2011 surge

After the Asian Financial Crisis and a prolonged slump, foreign buying reignited from 2005 onwards. A confluence of factors drove the surge:

Two integrated resorts (with casinos) announced — raising Singapore's global profile

Sentosa Cove launched — a rare opportunity for foreigners to buy landed property

Liberal immigration policies — the non-PR foreigner population grew 75% between 2005 and 2011

Low interest rates and quantitative easing post-GFC.

The numbers tell the story:

In 2011, foreigners — including both Permanent Residents and non-PRs — bought nearly one in three private condominiums sold in Singapore.

More significantly, non-PR foreign buyers alone surged from just 5.4% of the market in 2001 to 19.4% in 2011.

The tipping point

The 2011 boom was different from 2007. This time, foreigners were not just buying in the luxury Core Central Region — they were buying in the suburban mass-market (OCR) , the traditional heartland of Singaporean homeownership.

As The Business Times reported: "The strong encroachment of foreign buyers into the suburban private housing mass-market, which is the mainstay of Singaporeans, triggered the introduction in December 2011 of the ABSD".

Locals began to feel they were competing with wealthy foreigners and worried about being priced out of their own market.

The government acted. Since then, the government has raised ABSD for foreigners multiple times since its introduction in December 2011. Each hike made foreign buying more expensive.

Source: IRAS – History of ABSD rates

Case study: Country A vs USA citizen

Consider two buyers looking at the same S$2 million condominium.

One is a citizen of Country A. He pays 60% ABSD. His total upfront is over S$3.2 million.

The other is a citizen of the United States. His total upfront is roughly S$2 million — the same as what a Singaporean pays.

Same flight. Same property. Same weekend. Completely different outcome.

Why? Because of agreements Singapore signed with certain countries decades ago. These agreements are binding. The government has stated it has no plans to change them.

The US is not the only country with this arrangement. But it is the largest.

It's not a loophole. It's policy.

For eligible buyers, the benefit is claimed upon application. No special visa required. No minimum stay. No local partner.

For everyone else, the 60% rate applies.

What else works in your favour

No capital gains tax — you keep your profit when you sell

Strong legal system — English common law, state‑guaranteed title

Stable currency — the Singapore Dollar is managed to preserve value

Rental income — taxable at a flat rate, with deductions allowed

The details matter. But the headline is simple: for the right buyer, Singapore is still one of the best wealth storage destinations in the world.

Who is still buying?

Beyond citizens of certain countries, only two other foreign buyer profiles remain active:

Those who obtain Permanent Residence first

The ultra‑wealthy who treat 60% as a cost of entry

Everyone else has been filtered out by policy.

The bottom line

The 60% ABSD did not kill foreign buying.

It filtered it.

Whether you can still buy on attractive terms depends on three things: who you are, where you are from, and what you intend to do.

If you are a US citizen — the door is still wide open.

If you are not, there may still be pathways. Permanent Residence is one. The Global Investor Programme is another. But the window is narrower than it used to be.

City of Blocks

City of Blocks

Understanding Singapore Property Market, One Block at a Time

Newsletter

© 2026. City of Blocks - Brandname of QVB Holdings Pte Ltd All rights reserved.

Terms and Conditions